TL;DR:

- Fintech AWS migration involves moving workloads to the cloud for elastic capacity, lower costs, and regulatory compliance.

- Success depends on thorough inventory, compliance mapping, and automated security controls before migration begins.

Fintech AWS migration is the process of moving financial services workloads, data, and applications to Amazon Web Services to gain elastic capacity, lower infrastructure costs, and meet tightening regulatory requirements. The industry term for this broader shift is cloud migration for fintech, and it covers everything from rehosting legacy payment processors to refactoring core banking systems into microservices. Two forces are accelerating the timeline in 2026: regulators now mandate live resilience proof, and AI-driven development compresses app delivery from 365 days to 76 days while cutting required team size by 85%. Teams that migrate first capture that speed advantage. Teams that wait inherit the compliance debt.

What prerequisites does fintech AWS migration require?

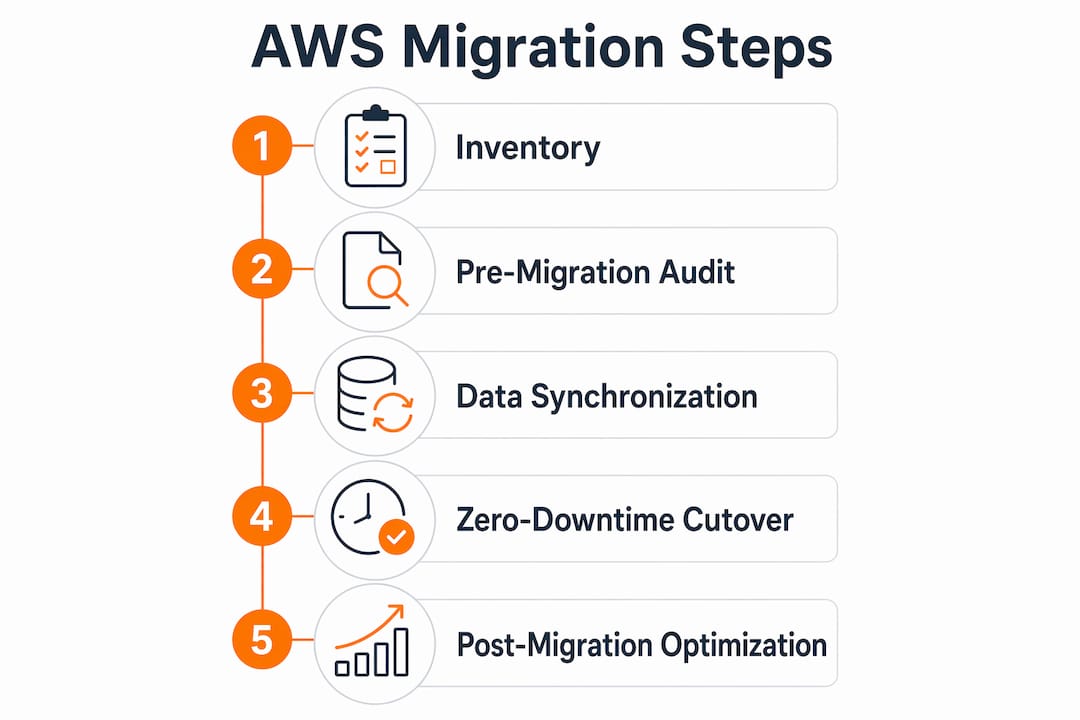

A successful migration starts with a thorough infrastructure audit, not a cloud account. Before moving a single workload, you need a complete inventory of every service, database, and integration point, along with its data classification and regulatory sensitivity. Skipping this step is the single most common reason fintech migrations stall six months in.

Three categories of preparation matter most:

- Compliance baseline. Map every workload to its governing regulation: PCI DSS for card data, SOC 2 for operational controls, and any jurisdiction-specific rules such as GDPR or FFIEC guidance. Document which workloads touch regulated data before touching infrastructure.

- AWS tooling selection. AWS Migration Hub tracks progress across services. AWS Database Migration Service handles relational and NoSQL data moves. AWS Config enforces configuration compliance continuously after cutover.

- CI/CD and security gating. Effective AI-driven development in financial cloud migration requires investing in CI/CD, automated security scanning, and audit controls before you write a single migration script. Without these foundations, AI-generated code ships faster but breaks compliance faster too.

Pro Tip: Run a pre-migration AWS security checklist against every workload tier before you begin. Catching a misconfigured IAM role in pre-migration costs minutes. Catching it post-cutover costs hours of incident response and a potential regulatory notification.

| Prerequisite | Tool or standard | Purpose |

|---|---|---|

| Workload inventory | AWS Migration Hub | Tracks all assets and migration status |

| Data classification | PCI DSS, SOC 2 | Identifies regulated data before move |

| Security automation | AWS Config, IAM | Enforces compliance continuously |

| Pipeline readiness | CI/CD with security gates | Prevents non-compliant code from deploying |

How can fintechs execute a zero-downtime AWS migration?

The answer is incremental extraction, not a big-bang cutover. The Strangler Fig pattern is the proven method: you build new AWS microservices alongside the legacy system, route traffic gradually, and retire the old components only after the new ones prove stable. One mainframe-to-AWS case study showed this approach produced 5x faster feature delivery with zero customer session loss. That result is not accidental. It comes from disciplined sequencing.

Follow these phases in order:

- Identify the extraction candidate. Start with a bounded, low-risk domain such as account inquiry or notification services. Avoid payment settlement as a first target.

- Deploy Change Data Capture (CDC). Use Kafka-based CDC streaming to keep the legacy database and the new AWS service in sync. Transactional outbox and CDC streaming maintain data parity and prevent drift across multi-year migration phases.

- Route traffic with a feature flag. Send 5% of traffic to the new service, monitor error rates and latency, then increase incrementally. Never flip 100% at once.

- Enforce identity-first security. In a perimeterless cloud, just-in-time IAM credentials replace perimeter firewalls as the primary compliance control. Automate credential rotation and scope every role to the minimum required permission.

- Run chaos engineering before go-live. 2026 regulations require fintech cloud failover systems to recover in under 60 minutes as demonstrated by live chaos tests. Schedule a formal game day before each phase cutover, not after.

Pro Tip: Treat each Strangler Fig extraction as a separate project with its own rollback plan. A clean rollback path for each phase removes the pressure that causes teams to push through warning signs.

| Migration phase | Key technique | Compliance checkpoint |

|---|---|---|

| Data sync | Kafka CDC + transactional outbox | Verify zero data drift before traffic shift |

| Traffic routing | Feature flags, weighted routing | Monitor error rates at each increment |

| Security | Just-in-time IAM, AWS KMS | Automated credential rotation active |

| Resilience proof | Live chaos engineering | Failover completes in under 60 minutes |

What challenges arise during fintech AWS migration and how do you fix them?

Connectivity failures are the most disruptive and least anticipated problem. Payment workloads maintain persistent TCP sessions, and cloud environments introduce idle timeout policies that silently drop those sessions. The result is reconnection storms that spike latency and trigger false fraud alerts.

AWS PrivateLink solves the core problem. Persistent session hardening with AWS PrivateLink and dedicated resource gateway health monitoring prevents the edge-case connection failures that take down payment infrastructure. Pair this with connection pool keep-alive settings tuned to your specific timeout thresholds.

Three other challenges appear consistently in fintech platform migrations:

- Data drift during phased rollout. When legacy and new systems write to separate databases, records diverge. Atomic updates enforced through the transactional outbox pattern keep both sides consistent until the legacy system is fully retired.

- Platform control versus speed to market. Building everything custom on AWS gives maximum control but takes longer. Using managed SaaS cores for commodity functions such as KYC or ledger accounting and reserving custom code for differentiating features is the faster path. Legacy software integration challenges are well documented, and the trade-offs between incremental and full migration are worth reviewing before you commit to an architecture.

- Regulatory exit strategy gaps. Regulators increasingly demand documented, tested cloud exit strategies that prove workload mobility within defined timelines. Automated, provider-agnostic deployment configurations satisfy this requirement and cost little to maintain.

Regulators do not accept theoretical exit plans. They want a runbook, a tested timeline, and evidence that your team has executed it at least once in a non-production environment. Build that capability before your next audit, not during it.

How do you optimize costs and scale after migrating to AWS?

Post-migration cost control starts with consumption-based pricing. Cloud core infrastructure is typically 60% cheaper than legacy MIPS environments. That gap exists because mainframes charge for every CPU cycle regardless of demand, while AWS charges only for what you use. The savings are real, but they require active management to capture.

Key practices for cost and performance optimization after migration:

- Rightsize continuously. AWS Compute Optimizer analyzes utilization patterns and recommends instance changes. Run it monthly, not once at launch.

- Containerize with AWS EKS. Cloud-native architectures on AWS deliver faster product cycles and consumption-based scaling on Kubernetes. Fintechs that lift and shift without containerizing leave most of the performance benefit on the table.

- Recycle idle nodes automatically. Schedule non-production environments to shut down outside business hours. This alone cuts compute spend by a meaningful margin for most teams.

- Use Savings Plans for predictable workloads. Payment processing and core banking have predictable baseline loads. Commit those to AWS Savings Plans and use On-Demand capacity only for burst traffic.

The architectural shift from legacy to cloud-native also accelerates product delivery. Teams that cut costs and boost scalability through AWS EKS and microservices ship features in days rather than quarters. That speed compounds over time and becomes a competitive advantage that no amount of mainframe tuning can replicate.

Key Takeaways

Fintech AWS migration succeeds when teams combine incremental extraction patterns, identity-first security, live resilience testing, and consumption-based cost management into a single disciplined program.

| Point | Details |

|---|---|

| Audit before migrating | Complete a full workload inventory and compliance mapping before touching infrastructure. |

| Use the Strangler Fig pattern | Incremental extraction produces zero downtime and 5x faster feature delivery versus big-bang cutovers. |

| Enforce just-in-time IAM | Identity-first security with automated credential rotation is the primary compliance control in a perimeterless cloud. |

| Prove failover live | 2026 regulations require chaos engineering tests that demonstrate recovery in under 60 minutes. |

| Capture cost savings actively | Cloud core infrastructure costs roughly 60% less than legacy mainframes, but only with continuous rightsizing and containerization. |

What I have learned from fintech migrations in 2026

The biggest mistake I see fintech teams make is treating the cloud as a destination rather than a discipline. They complete the migration, close the project, and stop there. Six months later, costs have crept back up, a compliance audit surfaces a misconfigured role, and the team scrambles.

The teams that get lasting value from AWS do one thing differently: they invest in the fundamentals before chasing AI-driven gains. CI/CD pipelines, automated security gating, and audit logging are not glamorous, but they are the infrastructure that makes everything else work. AI-assisted development can compress delivery timelines dramatically, but only when the underlying controls are already in place. Without them, you ship faster into a compliance problem.

My other strong conviction is that incremental extraction is not just a technical preference. It is a risk management strategy. Every big-bang cutover I have seen in fintech has produced at least one incident that required a weekend war room. The Strangler Fig pattern removes that pressure by making each phase independently reversible. Regulators also respond better to teams that can show a phased, documented migration history than to teams that executed a single high-risk cutover.

The regulatory direction in 2026 is clear: live proof of resilience, documented exit strategies, and identity-first controls are table stakes, not differentiators. Teams that build these into the migration process from day one avoid the expensive retrofit that teams who skip them always face eventually.

— Oleksandr

AWS migration expertise built for fintech compliance

Fintech organizations face a specific combination of pressures: regulatory deadlines, zero tolerance for downtime, and the need to cut infrastructure costs without sacrificing performance. IT-Magic addresses all three through a full-lifecycle approach that covers infrastructure audit, migration strategy, hands-on execution, and post-migration optimization.

As an AWS Advanced Tier Partner with 700+ completed projects, IT-Magic specializes in complex, high-load fintech environments where a misconfigured IAM role or a dropped payment session translates directly into lost revenue. The AWS migration services portfolio includes PCI-DSS-ready architectures, Strangler Fig extraction programs, and chaos engineering validation to meet 2026 recovery mandates. If your team is planning a fintech platform migration and needs a partner who takes full ownership of outcomes, explore the AWS for fintech service page or request an infrastructure assessment.

FAQ

What is fintech AWS migration?

Fintech AWS migration is the process of moving financial services applications, data, and infrastructure from on-premises or legacy systems to Amazon Web Services. The goal is to gain elastic capacity, reduce costs, and meet regulatory compliance requirements.

How long does a fintech AWS migration take?

Timeline depends on workload complexity and the migration strategy chosen. Incremental Strangler Fig migrations typically run in phases over several months, while simpler rehost migrations can complete in weeks.

What AWS tools are used for fintech data migration?

AWS Database Migration Service handles relational and NoSQL data moves, AWS Migration Hub tracks overall progress, and Kafka-based Change Data Capture maintains data parity between legacy and new systems during phased migrations.

How does AWS meet fintech regulatory requirements?

AWS provides PCI DSS-compliant infrastructure, AWS Config for continuous configuration enforcement, and IAM for just-in-time credential management. 2026 regulations also require live chaos engineering tests proving failover under 60 minutes, which AWS environments support natively.

What is the biggest risk in fintech cloud migration?

Data drift and connectivity failures are the two most damaging risks. Transactional outbox patterns prevent data drift, while AWS PrivateLink with persistent session hardening prevents the idle timeout failures that disrupt payment infrastructure.